In the mid-1990s, interest rates offered on guaranteed investment certificates (GICs) ranged from 6% to 8% per year for five-year terms. Those rates – generous by today’s standards – were a far cry from the double-digit rates available just a few years earlier; and far below the robust returns that stock market investments were kicking out at the time. This prompted GIC investors to deploy matured proceeds into mutual funds. Those savers-turned-investors were called “GIC refugees” because it was the first time many invested in anything other than popular term deposits.

I heard more than a few times a sentiment along the lines of, “if rates go back up to x%, I will move everything to GICs”. The “x” was the rate that was meaningful for each individual – usually two to three percentage points above the then-current rate. Today’s rates – which range from 4% to 5% depending on the term – are prompting many to desire the simplicity and safety of GICs to escape the ups and downs of stocks and bonds. This is especially so after the rough two years for bond markets.

So why do I pooh-pooh this simple savings instrument?

GICs are illiquid

I am not opposed to investing in less liquid investments if they offer higher returns to compensate for that illiquidity. With GICs, you get all of the inconvenience of illiquidity (until maturity) with little to no additional return in many cases. The most common reasons for wanting the flexibility to sell at any time are unexpected expenses or to rebalance a portfolio during a bear market for stocks. GICs are locked-in and cannot be sold before maturity. While cashable GICs are available, rates are less attractive.

GICs do not benefit from falling rates

When rates rose over the past two years, those holding GICs were happy to see steady values while bond prices declined. But when the reverse happens – i.e., falling rates – bonds will see a nice bump up in price. That higher price can be realized by selling a bond. Related to my first point, this is most important when stocks are falling. The ability to sell a bond allows investors to capture the capital gain caused by falling rates; and use the proceeds to buy downtrodden stocks.

Bonds are more tax-efficient than GICs

While it is not shocking to hear that GICs are not tax-efficient, many may be surprised to know that most bonds are more tax-efficient today than GICs. Here is an example to illustrate.

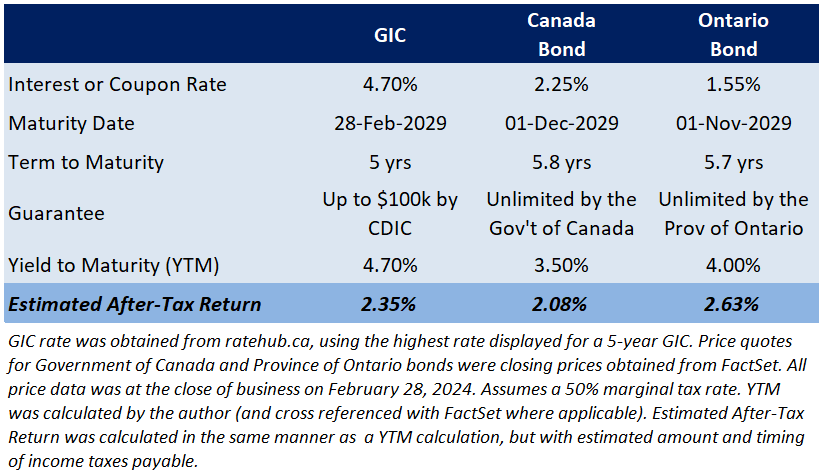

The GIC best rate I found recently was 4.70% per year for a five-year term. For the bond comparison, I selected bonds issued by:

- the Government of Canada (with a 2.25% coupon maturing on December 1, 2029); and

- the Province of Ontario (with a 1.55% coupon maturing on November 1, 2029).

The Canada bond had a recent yield to maturity (YTM) of 3.50% per year; which is, simplistically, the 2.25% annual coupon interest plus the capital gain on maturity (because it will mature at a price above its quoted market price). Similarly, the Ontario bond’s YTM was around 4% recently. When comparing the headline GIC rate with the bonds’ respective YTMs, the GIC looks like a no-brainer. But the after-tax picture is quite different.

The GIC’s 4.70% rate pre-tax gives it an advantage of 1.2 and 0.7 percentage points per year, respectively, compared to the Canada and Ontario bonds. But the GIC’s estimated after-tax ‘yield’ is just 0.27 percentage points higher than the Canada bond – and 0.28 percentage points lower than the Ontario bond. The table below summarizes the results of my calculations.

The GIC’s higher after-tax yield still puts it ahead of the Canada bond, in my view. But it’s not enough additional yield to compensate for its weaker guarantee (deposit insurance vs direct backing of the Canadian government), illiquidity (the bond can be sold at any time), and the ability to realize a gain if rates fall before maturity.

But if you must

If my arguments have not compelled you to avoid GICs, make sure you:

- use online rate comparison tools get a competitive rate;

- verify whether the quoted rate is simple or compounded (i.e., a 4.70% ‘simple rate’ equates to a 4.31% average annualized compounded return);

- use GICs mainly for registered accounts (e.g., registered retirement savings plans, tax free savings accounts);

- clarify the nature and limits of guarantees of any GIC you are considering (some regional credit unions offer high rates and provincial guarantees); and

- limit how much of your portfolio is in GICs to make sure you do not limit your liquidity or investment flexibility.