An outsourced Chief Investment Officer (CIO) is a fiduciary adviser with legal accountability to protect your assets and advise you objectively about inherent opportunities and risks associated with various investment options.

Once you have established your investment goals, an outsourced CIO helps you determine how to deploy your assets, designs your investment portfolio to meet your needs and reflect your risk tolerances, and selects and monitors the professionals who manage the portfolio on a daily basis.

Back to TopA wealth steward is someone placed in a position of trust to protect, oversee, and be responsible for the wealth of another.

In our view, wealth stewardship operates according to four key principles:

These Stewardship Principles are prudent and sound yardsticks by which both the mindset and actions of all wealth advisors (i.e. financial stewards) should be measured, to ensure that clients’ hard-earned wealth is protected.

Back to TopThe term objective refers to the fact that the decisions we make on behalf of a client are always in the client’s best interest as opposed to HighView’s – which aligns with our fiduciary duty. HighView has structured itself in such a way that we are financially indifferent as to which investment solutions are used in client portfolios. In other words, we do not make more or less money by using one investment solution versus another. This allows us to provide advice that is truly focused on client needs.

The advice that HighView offers is independent because it is not subject to potential conflicts of interest. We have no financial or other ties to any of the suppliers – including the investment managers – that we use.

Back to TopOpen architecture means that we do not use any of our own investment products. Instead, HighView carefully selects unaffiliated third party investment managers to manage the various components of our clients’ portfolios. We partner with these third party investment managers, which meet our strict criteria only after a thorough search and due diligence process. Once hired, we then monitor each manager closely and make changes as required over time.

In addition to hiring the most appropriate investment manager for each investment mandate (e.g. Canadian small cap equity, or Global mid-to-large cap equity), we also negotiate fees with each of these managers at the time they are hired. Typically the fees agreed to are designed to go lower over time as the total assets provided to each manager from all HighView clients increase. These fee savings are passed on directly to our clients.

Back to TopThese standards refer to the legal standard of care owed to clients.

The suitability standard requires that any recommended investment be suitable given the client’s circumstances. For example, if an investor seeks advice on how to invest to generate income, any product that generates income or has a reasonable yield will satisfy the suitability standard – regardless of the product’s cost or quality. All mutual fund dealers (i.e. regulated by the Mutual Fund Dealers Association of Canada or the MFDA), investment dealers (regulated by the Investment Industry Regulatory Organization of Canada or IIROC), and exempt market dealers are held to the suitability standard. Some individuals licensed under IIROC dealers are also held to a fiduciary standard.

A fiduciary standard, by contrast, requires any investment recommendation to be both suitable and in the client’s best interest. For example, the adviser to the above hypothetical income investor not only needs to make sure that investments recommended are suitable; but the adviser must also be diligent about finding, in the adviser’s assessment, the best products available to help the client achieve their goals. Firms registered as Portfolio Managers are held to a fiduciary standard. Accordingly, portfolio management firms must not only recommend what’s suitable for clients but also what is best.

HighView Asset Management Ltd is registered in the category of Portfolio Manager in Ontario and some other jurisdictions. You can check the registration of every firm in Canada at Canadian Securities Administrators registration check website. You can find HighView’s registration by clicking here.

Back to TopHighView Financial Group, through its wholly-owned subsidiary HighView Asset Management Ltd. is registered as a Portfolio Manager with the provincial securities commissions of Ontario, British Columbia, Alberta, Saskatchewan, and Manitoba. As a Portfolio Manager, HighView has a fiduciary duty to act with care, honesty, and good faith, always in the best interest of clients. Investment decisions are therefore independent and free of bias.

HighView is also a member of the Portfolio Management Association of Canada (PMAC). Established in 1952, PMAC is a forum for Portfolio Management firms to share best practices and industry knowledge. PMAC currently represents over 200 portfolio management firms who collectively manage more than $1.4 trillion of assets on behalf of pension plans, foundations, non-profit organizations, institutions, and high net worth investors. You can check the registration of every firm in Canada at Canadian Securities Administrators registration check website. You can find HighView’s registration by clicking here.

Back to TopPortfolio Managers such as HighView charge a percentage of the investments they manage. This fee is transparent and generally much less than retail management and distribution costs, which are often embedded as a cost of doing business. Fees are fully transparent on client statements and typically go down as a percentage of your portfolio as your assets grow. Fees are not paid by commission based on volume of buying or selling investments and are generally significantly lower than typical mutual fund fees.

It’s important to note that your money must reside at a custodian financial institution for an extra layer of protection and safety and there is usually a small additional fee for this service.

Back to TopThe primary safeguard that HighView provides to our clients is that, as a Portfolio Manager, we do not have custody of our clients’ investment assets. Instead, a separate financial institution establishes an account with each of our clients to hold and safeguard the assets contained within their portfolio.

This means that only the client can withdraw assets from their portfolio, and HighView – as Portfolio Manager – is only authorized to manage the assets contained within each client’s custodial account. For more information on this topic, please click here.

Additionally, firms such as HighView, who are registered as Portfolio Managers, must meet strict financial reporting, capital, and insurance requirements to further protect your investments.

Back to TopGoals-based investing addresses the holistic well-being of the family or foundation and directs transparent dialogues about ambitions, fears, and opportunities. It focuses on recommending appropriately designed solutions to achieve goals, tracks progress towards those goals, and adjusts the portfolio as necessary.

Goals-based investing is at the core of HighView’s investment philosophy, rather than the traditional industry model of measuring expected return versus market indices, which steers away from client goals and risk tolerance. Instead of asking “how can we increase returns or consistently beat the market?”, we ask “how can we achieve our investment goals with some degree of certainty?”.

This places performance in the context of achieving goals as the measure of success. Portfolio construction and investment performance is discussed in light of investment goals and risk tolerance as opposed to market dynamics. Ideally goals-based investing comes down to understanding the “purpose” of the funds, taking into consideration the levels of risk tolerance, the different investment horizons or liquidity constraints, and then focusing not on the gain or loss of the portfolio but on the probability of the portfolio to meet the financial and investment goals.

Back to TopMost of our Investment Policy Statements for family clients range from 15-17 pages, depending upon the complexity of each client’s situation. An IPS has key five sections:

The IPS should be carefully designed to meet the real needs and objectives of the client.

Back to TopAn Attitudinal Risk Assessment questionnaire is an essential tool that allows us to determine and understand a client’s acceptance and attitude about risk.

Risk is a very personal matter and as such must be assessed against an individual’s personal knowledge and past experiences. In order to gain an informed perspective, we have worked with a psychologist/cultural anthropologist to define the four dimensions of risk that must be considered and scored to establish a framework that can be employed when designing a portfolio solution for a client.

These dimensions of risk include:

Our questionnaire is scored through these four dimensions of risk with appropriate weightings given to critical elements, such as capacity. The results of this questionnaire are then married with the defined goals, flowing out the Wealth Planning process, which allows us to design a portfolio solution that aligns with the goals and behaves in a manner that provides our clients with the comfort and confidence they desire.

Back to TopAt HighView Financial Group, we believe that affluent Canadian families – whether they realize it or not – are actually operating a ‘wealth management business’.

In other words, their investable asset base is of a sufficiently significant size and complexity that it is beyond being considered a traditional savings pool earned from employment activities; it should instead be viewed as a wealth management business that is a bi-product of their successful business activities.

Over many decades of advising families of significant means, our experience has been that each family has unique levels of complexity which have evolved over the family’s evolutionary lifecycle. These complex structures are needed to address the delicate balance that exists between tax and estate matters, asset protection and income splitting issues, as well as current lifestyle versus longer term succession and philanthropic goals.

A truly integrated wealth plan eases some of this complexity and closes the gaps between the various elements of these structures, providing a solution that offers confidence and peace of mind.

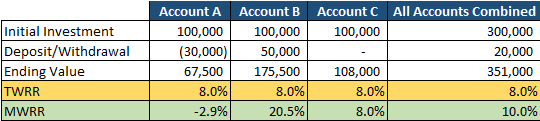

Back to TopIn our quarterly client reports, we use both the MWRR and the TWRR calculations for performance reporting.

First we use the money-weighted methodology to inform clients of the returns that were earned by each of their accounts and their consolidated portfolio.

Then, we show the performance of each of the investments owned within the portfolios using the time-weighted methodology, as this provides a more accurate reflection of how the underlying investment managers performed, excluding the impact of deposit or withdrawal decisions made by the investor.

Our examples below will highlight the differences between TWRR and MWRR:

Let’s assume that an investor has three separate investment accounts.

At the beginning of the year, she invests $100,000 into each account and makes the exact same investment in each account. In the first 6 months the underlying investment loses 20% and in the final 6 months of the year the underlying investment rises by 35%.

Let’s also assume that the investor withdraws $30,000 from the first account and deposits $50,000 into the second account immediately after the first 6 months.

The table below provides an example of both the TWRR and the MWRR of each of these three accounts and the total of all three accounts over the 12 month period:

The TWRR is the same regardless of the deposits or withdrawals because it measures the underlying investment’s return.

However the MWRR measures the investor’s performance. Accordingly, MWRR is heavily influenced by the dollar amount and timing of the deposits or withdrawals.

Account B, for example, had a significant deposit right before the investment rebounded – so it had more money benefiting from the rebound. The opposite occurred in Account A. And with no deposits or withdrawals the MWRR for Account C was identical to the TWRR.

When using MWRR, it is much more difficult to compare the performance of various accounts.

Back to TopA Virtual Family Office (VFO) is a family office model that harnesses the experience, dedication, and loyalty of your established group of independent advisors to provide the comprehensive wealth stewardship affluent families require. This model simplifies all important financial decisions, as decisions are made in a disciplined manner with the appropriate advisors, at the same table, all working together.

A VFO will help you navigate the challenges that come with wealth, including:

Integrated, holistic, and with only your family’s interests at heart, your VFO works together to create a seamless approach facilitated through well-defined governance, structure, and processes.

At HighView Financial Group, our response to the requirement for a VFO is “The Family Stewardship Council”, which we organize and guide in the fiduciary oversight of your wealth.

Oakville - Corporate Office

231 Oak Park Blvd, Suite 207

Oakville, Ontario L6H 7S8

(905) 827-8540

1 (888) 827-8540