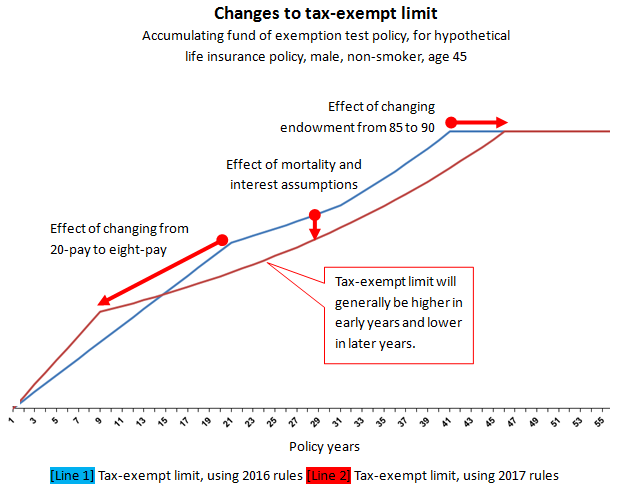

It will be almost three years in the making but Bill C-43 effective January 2017 will update 1982 tax laws. One of the benefits of permanent life insurance is that the money, while inside a policy, grows exempt from taxes. To remain exempt from annual taxation, the savings element must not exceed certain limits, set by tax legislation.

The government has now updated the rules to reflect longer life expectancy and to increase consistency across life insurance companies and products. Starting next year, the new rules will reduce the maximum amount of long-term tax-exempt savings allowed inside new policies. Existing policies will generally be ‘grandfathered’ from the new tax rules. However, some opportunities available in 2016 will no longer be available after December 31st. Other opportunities may not be as attractive as they are now.

In most cases, the tax benefits under the new rules will impact insurance planning for both personal and corporately held policies. It should also be mentioned that certain changes to ‘grandfathered’ policies after 2016 will result in the loss of ‘grandfathered’ status, meaning the new rules will apply.

Based on the new tax rules, some of the changes to life insurance policies at a high level are:

- Reduction in maximum tax-advantage growth over the long term

- Reduction in the additional deposit option for participating policies

- Lower NCPI (net cost of pure insurance) for standard lives, and therefore a lower collateral insurance deduction

- General, higher ACB (Adjusted Cost Base) for standard lives and for a longer period; meaning taxation on the death benefit of a portion of corporate policies

- Reduction in maximum amount that may be paid as premiums (impacts universal life more)

- Potential increase in the cost of insurance due to changes in computing the IIT (Investment Income Tax) on universal life policies

- The C.D.A. (capital dividend account) will be lower, which will affect the extraction of corporate funds

What’s not changing is the fundamental reason for buying life insurance: liquidity and protection in case of death. New products are being designed but not yet finalized that will continue to provide valuable tax benefits and growth opportunities.

If your family or your business requires a review of existing policies or life insurance as part of your overall investment portfolio, or if you need to put life insurance in place to meet other requirements, please contact HighView Financial Group to ensure you are maximizing your tax benefits as well as meeting your personal and business objectives to enhance your lifestyle and legacy goals/values.

*This material is for informational purposes only and should not be construed as accounting, legal, or tax advice. Reasonable efforts have been made to ensure its accuracy. All comments related to taxation are general in nature and are based on current Canadian tax legislation, which is subject to change. For individual circumstances, consult with accounting, legal, or tax professionals.

You may also be interested in: