At last, the year 2017 marks a great step forward for our country with regards to transparency and disclosure in the financial services industry.

The long anticipated regulation, that will impact Canadian investors, will be on display in many mailboxes and inboxes this month.

The Client Relationship Model (Phase II), or more popularly known as CRM2, aims to improve the level of information provided to Canadian investors. More specifically, investors will see what are they paying for the services provided by their financial advisors (or investment institutions) and how well their investments have performed.

This basic and necessary information is finally being brought out in to the open by our regulators.

Although it’s a giant step in the right direction for disclosure, we believe there are three areas of potential improvement for investor transparency:

- Insurance products are not covered by the rules and regulation of CRM2

- Charges and compensation report does not provide a full cost of ownership

- Performance reporting time frames are inconsistent across the industry

1. Insurance Products Are Not Covered by the Rules and Regulation of CRM2

Advisors selling insurance products, such as segregated funds, are not subject to the same transparency and disclosure as other investment advisors in Canada. Segregated funds, which are similar to mutual funds, are insurance vehicles sold by insurance agents and brokers; and therefore cause a competitive dilemma. For example, competitors within the financial services industry are now subject to different disclosure rules, which could lead to problematic scenarios for investors.

2. Charges and Compensation Report Not Providing a Full Cost of Ownership

One example of how the charges and compensation report will not provide a full cost of ownership: if an investment portfolio is made up of mutual funds (series A).

The average MER (Management Expense Ratio) for a series A stock fund in Canada is 2.5%.

The makeup of this MER is typically 1.5% to the sponsor for investment management and administration. The other 1.0% is provided to the financial advisor to select the fund and service the account.

This 1.0% advisor fee (or trailer) will be disclosed in the CRM2 compensation report, but the 1.5% will not.

The regulators agreed that since the 1.5% is already disclosed in the Fund Facts document, this was a sufficient amount of disclosure for now.

Unfortunately, a Canadian investor could incorrectly believe that the 1.0% fee disclosed in the report is all they pay for financial advice and service. When, in this example, the total cost of ownership is 150% more than their possible inaccurate assumption.

This scenario is common amongst many advisory firms who use all forms of investment funds, not just mutual funds, which is why a required full transparency on all fees and expenses in a summarized format would be highly beneficial for investors.

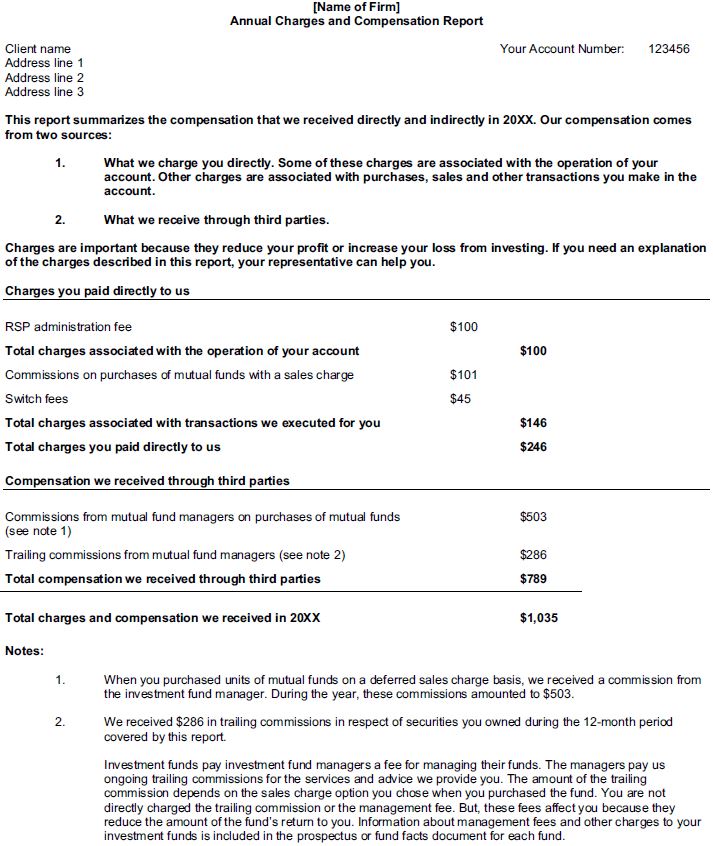

Enclosed is an example of a CRM2 Charges and Compensation Report set out by the Ontario Securities Commission that will be received by Canadian Investors1:

As stated in the document’s footnotes, information about management fees and other charges to your investment funds is included in the prospectus or fund facts document for each fund.

Unfortunately, the typical Canadian investor might not know where to find the applicable prospectus or fund facts, resulting in a lower level of disclosure than originally desired.

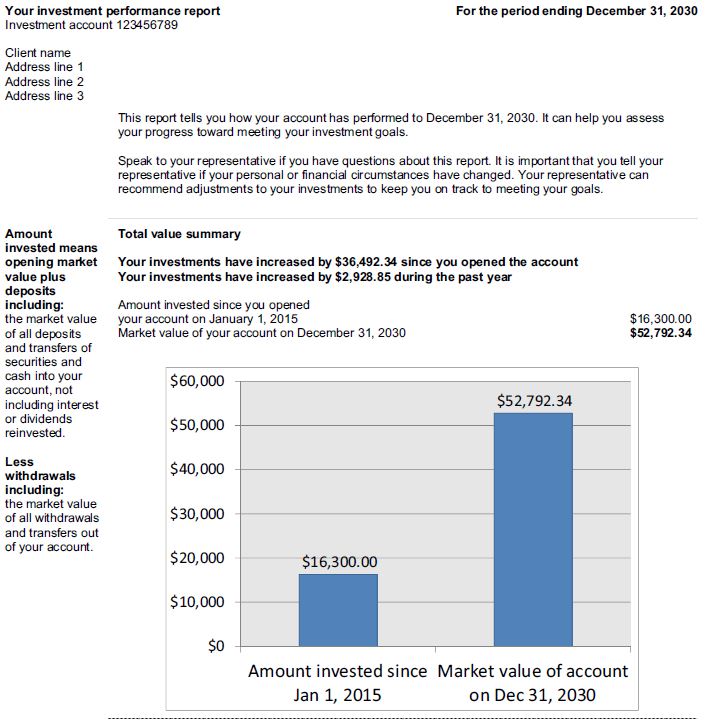

3. Performance Reporting Time Frames Inconsistent Across the Industry

With regards to reporting performance, the Canadian investment institutions that are forced to comply with CRM2 standards have been provided the flexibility to choose their own official start date for reporting.

For example, some institutions are providing performance figures from the inception of the client relationship, others are providing a five year rate of return (starting in 2011), or others are choosing 2009 and 2013 to remove the volatility of 2008 and 2011, respectively.

We believe that this is challenging for investors, as different time periods in capital markets (ie: start dated during up markets vs down markets) can provide material differences and biases in historical performance numbers.

Enclosed is an example of a CRM2 Performance Report set out by the Ontario Securities Commission that will be received by Canadian Investors1:

HighView Has Been Fully Transparent from the Beginning

At HighView, we act as a legal fiduciary for our clients. Our investment solutions and service are determined and provided with our clients’ best interests in mind.

Objectivity and transparency are also founding principles of our firm.

Objectivity provides our clients with peace of mind that there are no conflicts of interest present in our counselling relationship. We do not sell or manufacture our own investment products, which results in a level of independence and standard of care that is valued by our clients.

Transparency is on display every quarter for our clients with the delivery of our quarterly statements. Like many Canadians, they receive monthly statements providing them the value of their accounts at the end of each month, as well as a reconciliation of transactions and activity. At the end of each quarter, our clients also receive a portfolio review that provides a reconciliation of all performance metrics and fees within a quarter. The importance of carving out their advisory fee, investment management fee, and custody fee provides our clients the understanding of total cost of ownership. Our ability to separate the fees also maximizes the tax deductibility available to our investors.

The performance of the portfolio is also tied to each investor’s goals and objectives. As investments are just a utility, we want to be sure we are satisfying their short and long term obligations with the upmost prudence and care.

We applaud the efforts of the regulators and their persistence to make the Client Relationship Model (Phase II) a reality for Canadian investors and look for continued focus by regulators on the matters we’ve reviewed above.

Sincerely,

Reference

- Ontario Securities Commission, CSA Notice of Amendments to National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations and to Companion Policy 31-103CP Registration Requirements, Exemptions and Ongoing Registrant Obligations (Cost Disclosure, Performance Reporting and Client Statements) (2013), 42-44

If you would like to learn more about CRM2, we recommend you click on the following resources or call our head office. If you’re interested in our investment counselling services, please schedule a complimentary discovery session to see if we’re the right team for you.

CRM2 Videos:

CRM2 Blogs: