On July 15, 2016 the second phase of Client Relationship Management (CRM2) became official. CRM2 is a new set of rules requiring most “financial advisors” to provide two new annual reports to each client – one detailing amounts paid to advisory firms and another detailing performance. The performance report will show your investment accounts’ percentage returns.

On July 15, 2016 the second phase of Client Relationship Management (CRM2) became official. CRM2 is a new set of rules requiring most “financial advisors” to provide two new annual reports to each client – one detailing amounts paid to advisory firms and another detailing performance. The performance report will show your investment accounts’ percentage returns.

The following are important things to know when reviewing your CRM2 performance report:

Timing

Some firms’ recent statements are starting to show performance. But since most people like calendar year reporting, many firms will probably send the first round of CRM2 reports during the first part of next year.

Firms that scatter client reviews throughout the year will likely start sending their first performance reports very soon. The latest you can receive your first performance report is July 15, 2017.

Rates of Return

Rates of return that you see advertised for investments are calculated using a method called “time-weighted rate of return” (TWRR).

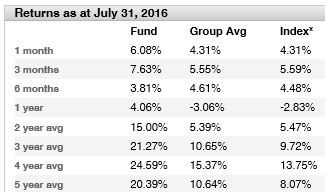

Below is a screenshot from a GlobeInvestor fund profile that shows, for example, that this fund generated an average compounded return of 15% per year for the two years through July 31, 2016. That is the fund’s TWRR return.

The only way an investor in that fund could have experienced that precise return is, for example, to have invested $10,000 in this fund on July 31, 2014, to have held it through July 31, 2016, and have done no buying or selling in the interim. In this case the value would have been $13,222 on July 31, 2016 (i.e. 15% per year).

But in the more common scenario goes something like this:

- buy $3,000 on July 31, 2014;

- buy $3,000 on February 18, 2015;

- buy $4,000 on February 29, 2016;

- hold through July 2016.

In this scenario, the same amount of money was invested in total but it was added throughout the two-year period – not all at the start. In this case, the ending value is $11,718 – and the CRM2 performance report would list the personalized return as 12.92% per year for the same two-years. It accounts for the fact that the initial $3k was invested for two years, the second $3k was invested for 17 months, and the final $4k instalment was invested for only five months.

This personalized number is referred to as a “dollar-weighted rate of return” (DWRR) because it factors in how much you buy or sell and when those transactions occur.

TWRR measures the product’s performance (i.e. not impacted by timing and amount of buys and sells). DWRR measures the investor’s performance. Most firms will simply report your personalized DWRR on your new performance reports. A minority of firms will show TWRR and DWRR.

Start Date Bias

End-date-bias is a term used to describe how measuring performance at the end of an extreme performance streak can be misleading. Examining 5-year returns, for example, at the bottom of a bear market or years into a robust bull market will not give you meaningful information. These return measurements are biased by the extreme recent moves. CRM2 performance reports risk the opposite type of bias.

I recently heard some industry chatter that a couple of firms are choosing February 27, 2009 as their performance start date. This is very near the universal Financial Crisis low. Since then, stocks have generally doubled in value through July of this year – while bonds are up nearly 40% in total. This start date is an indication of trying to inflate performance – which is disingenuous.

Using the date the account was opened is a far more sensible approach. But an advisor I know at firm using this approach lamented that most of his clients joined him in 2007 – just before the Financial Crisis. Other firms will choose a recent start date – e.g. covering just a year or two of total returns.

I know that many of you have accounts with two or three different advisors. Differences in start dates will make comparisons tricky so keep this in mind when reviewing your performance reports.

I also encourage you to read “A nasty eye-opener – performance reports may be unsettling” in Investment Executive.

HighView Financial Group is an investment counselling firm that takes a fiduciary approach to affluent family and foundation wealth. We are transparent and accountable in all that we do. Schedule a complimentary discovery session to see if we’re the right investment stewardship counsellors for you.

You may also be interested in: