I have been writing about investment products offering generous cash payouts for nearly twenty-five years. It is my favourite topic because investors have long been infatuated with investments that churn out monthly cash – and creators of investment products love to feed into this often-unhealthy obsession. I have written about covered call writing many times over the past decade.

More recently, I analyzed the claim that covered call strategies excel in flat markets. In my view – and that of many others smarter than me – this claim is largely a myth. But there is another often-cited claim worthy of analysis. Covered call strategies are not designed for raw outperformance, proponents say, but rather as reliable sources of tax efficient cash flow. Let’s put it to the test.

(For a refresher on how this strategy works, check out my May 2023 article.)

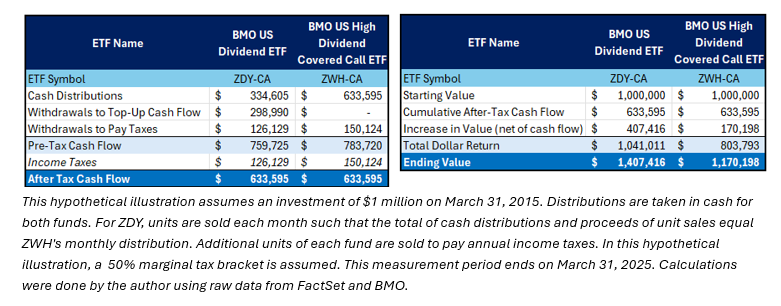

I created an illustration of two hypothetical investors using two similar BMO exchange traded funds (ETFs) that have been around for more than a decade. The BMO US High Dividend Covered Call ETF (ZWH) sells call options backed (or covered) by about a hundred U.S. dividend-paying stocks. The BMO US Dividend ETF (ZDY) employs a very similar strategy to its covered call sibling, except that it holds about eighty U.S. dividend paying stocks and does not use options or other derivatives to boost cash flow.

(I chose BMO because they have some of the oldest covered call products. And I chose ZWH and ZDY because they offer broad diversification in a category filled with sector-focused funds.)

My illustration compares investing one million dollars in each ETF and using each to generate cash flow for ten years. That means taking all monthly distributions in cash – not reinvesting them. The covered call ETF (ZWH) pays out more cash each month than ZDY, so we assume that the ZDY investor supplements the monthly cash payouts by selling some units every month. That way, each investor receives the same amount of cash each month.

I calculated capital gains on each hypothetical sale of units and used the tax breakdown of distributions to calculate annual income tax. And I assume that each investor sells units each April to pay the prior year’s tax bill – treating each fund as the investor’s main source of cash flow. The tables below summarize selected statistics from my illustration.

The table above-left shows that each investor has the same amount of after-tax cash flow. ZWH’s covered call strategy paid out more in pure cash distributions over a ten-year period but incurred a higher income tax liability. The table above-right shows that despite having to sell more units of ZDY to equate to the same cash flow level of ZWH, the investor in ZDY was left with a 20% higher market value at the end of the ten-year period (almost $240,000 higher for our hypothetical ZDY investor).

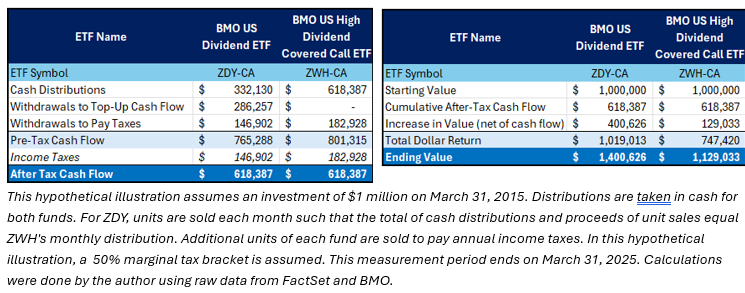

In my illustration, ZWH’s covered call strategy delivered a healthy amount of cash flow and kept capital intact. But ZDY put just as much jingle in its investor’s jeans, was more tax efficient, and produced a higher total return. On the chance that this was a fluke of this particular pair of ETFs, I repeated this analysis with a couple of other BMO ETFs – and the outcome was the same.

Covered call strategies are not so bad, but they are overhyped in my view. Every thoughtful analysis I have read – and all of the analysis I have done myself – points to an unattractive tradeoff.

Some covered call strategies are better than others in terms of upside exposure and tax efficiency. But they usually give up too much upside and are often tax-inefficient compared to pure and simple stock market exposure. Call me Danny Downer if you must, but I have yet to encounter a covered call strategy that I would buy or recommend to others – and I don’t see that changing any time soon.

{kind=link}