There are few investments that investors love more than those that spin out regular cash payments. One such strategy – Covered Call Writing – is attracting a lot of attention and investor dollars. Many investors view this strategy as generating extra yield. While it boosts up front cash flow, this strategy is not what investors think it is. That cash yield that seduces so many investors is not yield at all.

Option Basics & Covered Call Writing

Covered call writing involves buying shares of a company and selling options on those shares. Proponents claim that the premium revenue cushions stock price declines while adding to overall returns. There is just one problem. Financial markets do not give out free money. If you are receiving a benefit, there is always a tradeoff. If it’s not obvious, keep looking – because a tradeoff or additional risk exists.

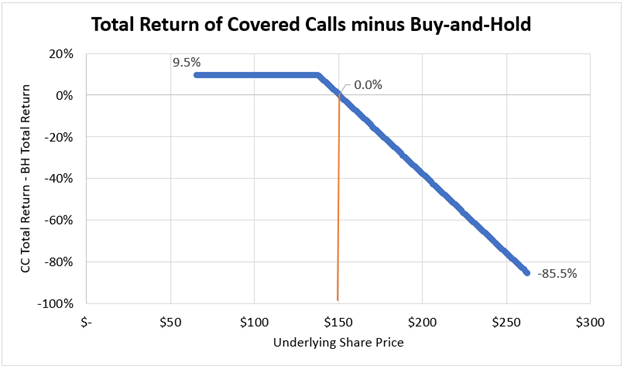

Let’s dig in using an example. At the time of writing, Royal Bank of Canada’s common shares traded at around $131 apiece. I found a Royal Bank call option on financial database FactSet with the following terms:

All of these figures change in real time during trading hours, but let’s freeze them in time for our illustration. Buying this option contract will cost $310 (the premium of $3.10 x 100 shares) for the right to buy one hundred shares of Royal Bank at $135 per share between now and July 21, 2023. Investors engaging in covered call writing will buy Royal Bank shares at $131 per share and sell the above call option.

The covered call investor (i.e., the option seller) can do this up to four times in the year using three-month contracts to collect $1,240 in this example ($310 x 4). Using these numbers, I calculated the return profile of two hypothetical investors over a range of share price scenarios over a one-year period.

The buy-and-hold investor (“BH”) buys one hundred shares of Royal Bank and holds them for a year. The covered call writer (“CC”) buys the Royal Bank shares and sells the above call option to generate extra cash flow. I used share price scenarios ranging from half of the recent $131 share price up to about double the recent price. I calculated total returns for each of those price points and for every price in between in $0.50 increments. The chart below plots the difference between total returns of CC and BH at each price point over a one-year period.

Note the following observations.

Fictitious Yield

Many investors view the cash flow that CC investors receive for selling the options as yield. While premiums provide cash flow, they are not yield. Rather, they are CC’s compensation today for a future liability to the option buyer to sell them the underlying shares. CC will often get lucky when the option buyer does not exercise their option – allowing CC to keep the premiums without having to sell shares to the option buyer. And this may well continue for quite a while – allowing CC to keep generating cash flow from selling options.

If investors like CC run their strategy long enough, however, the cost of having to sell underlying shares far below market prices will eventually far outweigh premium revenue. Accordingly, revenue from selling options is not income or yield. The result will eventually be only slightly less downside risk and volatility in exchange for significantly lower total returns.

Real World Performance

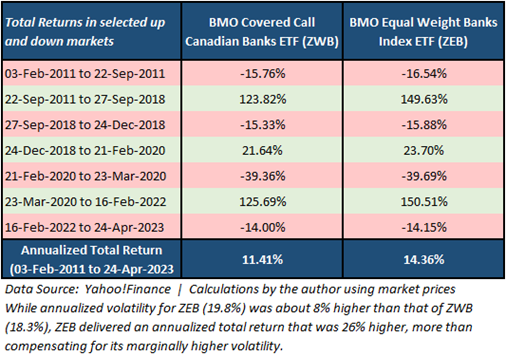

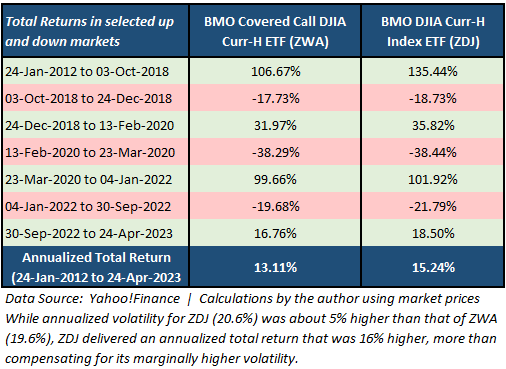

According to National Bank Financial, there are $17 billion invested across more than one hundred exchange traded fund (ETFs) listed on the Toronto Stock Exchange that use a covered call strategy. Most have less than five years of history. I calculated performance statistics for two of the older covered call ETFs – comparing each to a highly similar ETF holding only the underlying stocks (with no options).

In each case, the covered call funds have similar downside risk characteristics, modestly lower volatility, but significantly lower total returns. The below examples use two pairs of BMO ETFs. I’m not knocking BMO, but using their products to illustrate my points because they have some of the oldest covered call ETFs and the variety to make good comparisons.

Just as I argued above, the below covered call ETFs did not offer big protection in down markets; and they were only slightly less volatile than their non-covered-call peers. But this marginal risk reduction came at a steep price in the form of significantly lower total returns. In my view, investors should bypass covered call strategies and simply own stocks for their total return potential. The return given up with covered calls over time is too costly for the small short-term benefits received.

Regardless of how you acquired your wealth, there’s one thing all investors have in common—a…

An architect wouldn’t design a custom home for a family without first asking many questions…

Financial planning is the first step in a comprehensive discovery phase at HighView Financial Group.…

A “fixed asset” is a long-term tangible asset that is not expected to be consumed…

One of the core principles at HighView is to understand the purpose of the portfolio.…

{kind=link}

{kind=link}

{kind=link}